Insurance is a tricky maze where most people are confused on what they actually need. Who can we trust to give us the most unemotional advise without any sales talk or hard selling? Feeling pressured to buy any insurance is not the way to go. We have the right to really think about what we need without any hard selling.

With a digital "adviser", all the hard selling, and the pressure to buy are all gone. We can now assess our own insurance needs at the comfort of our homes, making decisions with a clear mind without any distractions.

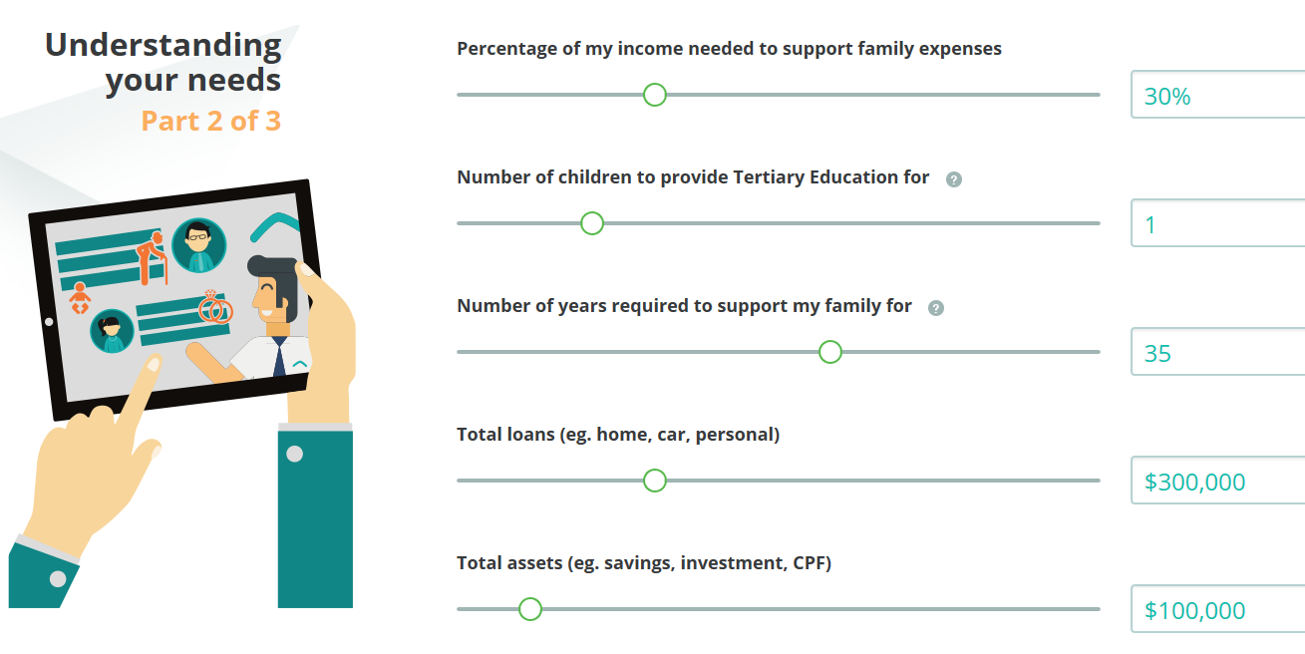

How Selfcheck works?

I've tried out this selfcheck and I would say I'm quite impressed at how easy it is to use and the quality of the recommendations which are given. I don't even need to spend 1 hour of my time to listen to sales talk. All it takes is just 5-10 mins to key in my personal data and then the system calculates my insurance needs and recommends the best insurance plan comparing various companies in the market. If you did not know, DIYInsurance is also an insurance comparison web portal.

My Selfcheck results

First, they will ask for some personal details such as your name, date of birth and annual income

After which, there will be some questions on assessing our financial needs and health.

Thirdly, will be some basic questions on our employment status and expectations

And lastly, the results are generated out

For my protection needs, the digital adviser recommended 4 main insurance:

- Death

- Critical Illness

- Disability Income

- Healthcare

If you realise, all the recommendations are for insurance needs only. There are no savings plans, endowment or investment link policies involved. This is in line with what I believe that insurance should just be for insurance coverage and not be complicated with savings or investment. I don't have to pay high fees to save and invest when I can do it myself at very low fees.

Honest advise and trusted service

Talking about fees, in case you did not know, DIYInsurance staff are not commission based which is very different from normal insurance advisers out there. They are all salaried base which means they do not get extra money from recommending any insurance plans you do not need.

However, the quality of service still maintains the same. There is a dedicated adviser assigned to each person and in the event of a claim, they can approach their adviser to process it. They also have a Client Service Management team to help on any needs which you may have.

Save on your insurance?

Because of the selfcheck digital adviser platform, processes become more efficient which allows DIYInsurance to pass on greater cost savings to their clients. They are increasing the rebate of agent’s commissions from 30% to 50% back to you. This is a straight 50% cost savings on the commissions which is paid to the company. As mentioned before, DIYInsurance staff are salaried so the commissions are actually paid to the company like a referral fee which all other insurance companies pay to their agent too.

As what I understand from them, the commission rebates are not just for 1 year, they are for as long as the insurer pays them (usually 3-6 years along). This is really a good initiative from them to pass cost savings to their clients.

DIYInsurance is MAS licensed since 2003 and is a trusted place to be insured. I've personally interacted with their staff before and know that they really want to serve people well. Try out the new selfcheck digital adviser and see for yourself the new era of financial advisory.

This article was written in collaboration with DIYInsurance. All views expressed in the article are the independent opinions of sgyounginvestment.blogspot.sg

Enjoyed my articles?

You can Subscribe to SG Young Investment by Email

As what I understand from them, the commission rebates are not just for 1 year, they are for as long as the insurer pays them (usually 3-6 years along). This is really a good initiative from them to pass cost savings to their clients.

DIYInsurance is MAS licensed since 2003 and is a trusted place to be insured. I've personally interacted with their staff before and know that they really want to serve people well. Try out the new selfcheck digital adviser and see for yourself the new era of financial advisory.

This article was written in collaboration with DIYInsurance. All views expressed in the article are the independent opinions of sgyounginvestment.blogspot.sg

Enjoyed my articles?

You can Subscribe to SG Young Investment by Email

or follow me on my Facebook page and get notified about new posts.