CNA came out with an article on Financial Independence, Retire Early (FIRE) and the writer really captured the gist of what financial independence is about. In fact, this is the first time I've seen such a good article from main stream media talking about financial independence. You can read the article here.

Image adapted from https://teenfinancialfreedom.com/

Financial advice from main stream media?

In the past, most financial advice from main stream media often comes from financial advisors or experts but are often not so relatable to the people on the street. Most advice will tell you to save certain amount and draw down that amount when you retire. For example, a typical advice will ask you how much you need per month during retirement (eg $5000) then you'll need to save $xx amount so that it can last you for xx number of years. If you save up $1 Million dollars, $5000 per month during retirement will only last you 16 years ($1 Million divided by $60,000/year). If you retire at 65, this $1 Million will last you till you're 81.

With articles on FIRE coming out from main stream media like CNA, it goes to show the younger generation of journalist have been brought up differently and are exposed to other forms of financial advice other than from experts alone. This is encouraging as more young people are taking charge of their own finances and are finally seeing the light to the real financial independence.

Financial Independence, Retire Early (FIRE) movement

The Financial Independence, Retire Early (FIRE) movement is different. This started to get more popular through the financial blogging community where a group of us were so called obsessed with saving enough to retire early. I was one of them back then when I started this blog in 2013. Its been 9 years of blogging journey and more than 10 years of pursuing financial independence for me. I was impacted by other bloggers who have been blogging for a few years and in fact, most of them have already achieved financial independence by the time I read their blog. A few of them were in their 40s and have accumulated millions and put their money to work over many years to achieve the financial independence they were able to enjoy. Although I don't write as much now, I'm still quite active in managing my own finances and still putting my money to work through investing. I've not given up on this journey and in fact I'm glad I started it early.

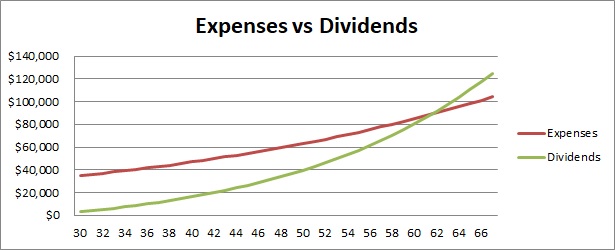

Achieving financial independence is defined as "the status of having enough income or wealth sufficient to pay one's living expenses for the rest of one's life without having to be employed or dependent on others." This definition I extracted it from Wikipedia. It accurately describes what FI is all about. The income to pay one's living expenses is often from dividends from stocks, rental from property, annuity plans (eg CPF life) etc. The key is this income must be passive. This is the method which I subscribe to as compared to traditional advise of asking you to save and then draw down your savings during old age. Drawing down your savings is also a form of retirement plan but you'll soon realise that many people face the problem of not enough money in their old age and have to go back to the workforce again even when they are in their 70s. Remember, $1 Million dollars can only last you 16 years if you draw down $5000 per month. That's not a lot of years to be honest for retirement.

Is it possible to retire early?

The FIRE movement has financial independence but also has retire early in its description. If you want to retire early, having the plan to draw down your savings when you retire is a definite failure. It won't work at all because your numbers of years to live will be quite long. For example if you retire at 50 and live till the age of 80, that's 30 years of life! If you spend $5000 per month for 30 years, that's a total sum of $1.8 Million dollars! Don't forget, inflation will still continue to happen for that 30 years and even at 3% inflation, $5000 will only be worth $2500 in 24 years. This is because at 3% inflation, your same plate of chicken rice at $4 will probably cost $8 in 24 years. If you think this is unlikely, look at how much the same plate of chicken rice was about 20 years ago? The answer is $2 and it has doubled to $4 now in 20 years or probably lesser as what we've experienced.

If you have passive income in the from of dividends or rental income, that income will increase over the years. Why is this so? Think about it, rental income has definitely increased over the years. I found from HDB website that the rental rates of a typical 4 room flat is about $2000-$2400 in 2022 while the rental rates was $1300-$1500 back in 2007 which is 15 years ago. This is a 50%-60% which is about 3%-4% increase per year which just nice covers inflation.

If you have passive income from dividends, the income also will increase over the years. That's if you pick the right stocks with growing dividends or what we call distribution per unit (DPU). Let's take a look at one dividend stock in Singapore which is Frasers Centrepoint trust. Its dividend in 2007 was only 0.066 cents per share and in 2021, its dividend is 0.12 cents. That's a whopping 82% increase over 14 years which is an increase of about 5.8% per year. That's even higher than the rental income growth from a HDB property. Although there's a significant drop in DPU in 2020, it has mostly recovered back and is on track to grow even more beyond 2022. Not only that, FCT share price has also increased from 1.29 during its IPO in 2007 to 2.32 now which is a 80% increase.

Is extreme savings needed to achieve FIRE?

Now comes the question, how do we achieve FIRE? Do we need to embark on a campaign of extreme savings to achieve what we want? In 2014, I wrote an article on "Why extreme savings is more powerful than investing". I was much focused on saving as much as possible back then and would scrimp and save even on food and drinks. I was brought up in an environment where money was hard to earn and saving as much money for rainy days is important. As I grow older, I begin to realise the importance of balancing saving vs spending. Its about setting a plan on not too much savings as well as not too much spending but still being able to achieve your financial goals. As I continue to invest my money and my dividends from stocks continue to grow, I'm able to spend more and still can achieve financial independence around the age of 47 which is 12 years from now. That's the goal I set for myself. This is the balance I seek where I don't achieve FI that early but don't have to scrimp and save every dollar I have.

I've also seen some people embark on Barista FIRE where instead of having enough passive income to support your lifestyle, you have the passive income to cover your basic needs and work part time to cover the rest. This can be called a semi retirement where you retire from full time job and work part time doing the things you like.

Enjoy the journey

A financial independence journey is often a long one so its important to enjoy the journey along the way. There are certainly some sacrifices to be made to save enough but its important to also balance and enjoy sometimes.

Enjoyed my articles?

or follow me on my Facebook page and get notified about new posts.